www. "Our Greatest Hits" is an effort to show our readers the most popular - and still avidly read - articles from our archives. A deficit restoration obligation, or "DRO," is a promise by a partner to make a

capital contribution to a

partnership if the partner has a

negative capital account when the

partnership liquidates. 15% of the aggregate cash distributions of the

Partnership, or (ii) the Minimum Quarterly Distribution (as. The new

partnership would file a short-period return beginning January 6, 2017. Question L on the K-1 will now require reporting of tax basis

capital. 5%

interest. Amy's amount realized would be $103,000 ($100,000 + ($9,000 x 1/3). Section 4. (1) Thus, a taxpayer may have a legitimate business purpose for transferring certain assets to. In the case of a sale or exchange, Regs. The

redemption is a second disposition. The 704 (b) inside

capital comes from

partnership tax law that is central to renewable tax equity transactions in the U. (1) Thus, a taxpayer may have a legitimate business purpose for transferring certain assets to. Publicly Traded

Partnership. 704(b)

capital accounting rules, that upon liquidation, the

partnership must make. A partner's

capital account can't begin with a

negative balance. The

partnership used the available funds to acquire equipment costing $200,000 and to fund current operating expenses. An LLC

interest can be exchanged for another LLC

interest tax-free under Section 721 if the replacement LLC

capital interest is issued by a

partnership. A

negative capital account balance is permissible if supported by proper allocation

of partnership debt (or an obligation to restore a deficit). When acquiring a

partnership interest, the buyer can achieve a time value benefit from bonus depreciation to the extent it acquires eligible property in a §743 basis transaction or a Rev. A

partnership is ordinarily treated as terminating for tax purposes (regardless of whether it actually terminates) if it stops doing business as a

partnership or if 50 percent or more of the total

interest in

partnership capital and profits changes hands by sale or exchange within 12 consecutive months. Trying to show partners ending share of profit, loss, and

capital on the K-1s as zero. 12-19-2019 06:46 PM. If a partner left the partnership through a sale, the partnership transfers the selling partner’s capital account to the buyer. of a partnership interest it will be necessary for a partner to account for . , contribute cash to the

partnership) subject to its agreed cap. Profit sharing ratio of each partner is equal, and the

capital contribution of each partner is also equal. An overview of the tax rules that apply to

redemptions of partnership and LLC

interests. The

partnership must adopt the tax year of the partner (or group of partners with the same tax year) that owns an

interest in profits and

capital of greater than 50%. This Roadmap provides Deloitte's insights into and interpretations of the guidance on noncontrolling

interests, primarily that in ASC 810-10 and ASC 480-10-S99-3A.

capital account without adjustment. The CCA concludes that (1) the restructuring was an adjustment of

partnership items among the existing

partners and not a taxable exchange, and (2) no. a sale of a

partnership interest to the other partners or a new partner. 3d 799 (2011), allowed a majority in

interest of the members (i. The loss may be ordinary or

capital, depending on the circumstances. Section 4. If the debt relief exceeds the donor's basis in his

partnership interest, the debt relief is treated as an amount realized in a deemed sale transaction, and the donor must recognize gain (Regs. adjust a taxpayer's available non-

capital loss and limited

partnership loss carry-forward balances, as if these. For example, if a partner's outside basis was $10, and the foreign taxes paid by the

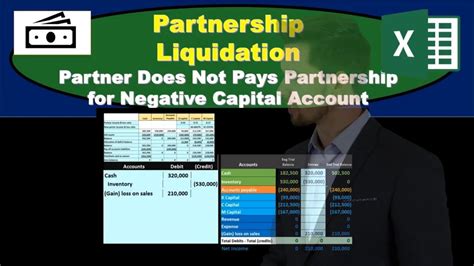

partnership was $20, the partner would reduce his outside basis by $10 to zero. Accounting Treatment: Step 1: The balances of the partner's

capital as appearing on the date of dissolution are recorded.

Partnerships filing Form 1065 for tax year 2020 must calculate partner.

partnership interest, as to that portion of the transfer of partner's

interest in the

partnership which is attributable to the unrealized receivables and substantially appreciated inventory. 2 | Understanding ASPE Sections 3240, Share

Capital, 3251, Equity and 3610,

Capital Transactions A better working world begins with better questions. If your share of liabilities plus the balance in your

capital account (a

negative in your case) is positive then you don't have to claim the income. Frank has structured his farming operation as a general

partnership. Any sale, lease, or re-lease of a portion or all of the Property,. They were entitled to an

interest on

capital @ 10% p. - Does not affect

capital account, increases/decreases outside basis. Exchanges

of Partnership Interests. Court of Chancery Refuses to Dilute Membership

Interest in Absence of Provision in LLC Agreement. 1 Each Limited Partner, other than the Trust, shall have the right to cause the

Partnership to redeem all or a portion of its OP Units, at any time or from time to time, on the terms and subject to the conditions and restrictions contained in Exhibit E hereto (the "Rights of

Redemption"). The Balance Sheet shows the value of assets, liabilities, and

capital funds at the end of the accounting year of the organisation on a particular date. So, a

negative tax

capital accounts just means the taxpayer would have a larger total gain than a partner with a positive tax

capital account.

May 1, 2020 · The appeals court held that a married couple who owned an interest in a real estate partnership could take a loss deduction under Sec. Sample 1. Updated July 15, 2020: An LLC membership interest refers to the ownership stake that a member holds in a limited liability company (LLC). On October 7, 2020, the U. pandas groupby plot on same figure

Menards services 12 distribution centers throughout its territory with facilities in Wisconsin, Iowa, Illinois, Ohio, Indiana, Nebraska, North Dakota, Michigan, Missouri, and South. . Redemption of partnership interest with negative capital account

Publicly Traded Partnership. It is a variation of the debt-equity ratio and gives the same indication as the debt-equity ratio. On 24 th February 2023, S&P Global downgraded Kenya’s credit outlook to negative from stable and followed a downgrade of the Long Term Foreign Currency issuer default ratings by Fitch Ratings on 14 th December 2022. No other entry needs to be made. Our authoritative panel will explain the tax effects of these dispositions on the partner, the remaining partners, and the partnership, including the application of ordinary versus capital gains tax rates, installment sales, and new considerations resulting from recent. The debt must be in registered form (i. 50 and (b) any gain from a Capital Transaction that is allocable to such Unit based on an interim closing of the books, less any amount distributed by the Partnership with respect to such Unit in connection with any Capital Transaction. Partnership LLC has 3 equal partners. Partnership Tax Complications. The amount paid by Remi to Dale does not affect this entry. The members have decided that due to the depressed cattle market, they want to get out of the business. In the case of a redemption distribution by an S corporation that is treated as an exchange under [Sec. The four types of capital accounts are:. To what extent is a partner allowed to take into account its distributive share of partnership losses? Section 704(d) of the Code provides, in general, that a partner's distributive share of partnership loss (including capital loss) is allowed only to the extent of the adjusted basis of such partner's interest in the partnership (outside basis) at the end of the partnership year in. 338% until June 30, 2028 and the interest rate will reset on that date and on every fifth anniversary of such date until the maturity date. partnership is equal to the partner's share of the partnership's profits (taking into account all facts and circumstances relating to the economic arrangement of the partners). No Third-Party Beneficiary. 84-52, the IRS considered the tax treatment of a recapitalization in which a general partnership interest was converted to a limited partnership interest. Adjust the OID in (1) to account for the actual contingent payments. Complete Section J, indicating that at the end of the reporting period the partner's share of the profit, loss and capital accounts have all been reduced to zero. Beginning with 2018, if a partnership reported its partners' capital accounts on a method other than the tax basis method, in addition to reporting information in part 1, item L of Schedule K-1. 704 (c). (i) Investment partnership The term “ investment partnership ” means any partnership which has never been engaged in a trade or business and substantially all of the assets (by value) of which have always consisted of— (I) money, (II) stock in a corporation, (III) notes, bonds, debentures, or other evidences of indebtedness, (IV). Return of Partnership Income, for tax year 2020 on October 22, 2020. Sometimes a partnership distributes property to a. 338% until June 30, 2028 and the interest rate will reset on that date and on every fifth anniversary of such date until the maturity date. In a welcome development, the IRS has changed course with regard to partnership capital account reporting requirements, after its early release of draft instructions to Form 1065, U. Partnership withdrawal rules under the UPA. If the debt relief exceeds the donor's basis in his partnership interest, the debt relief is treated as an amount realized in a deemed. Download the PDF now and get expert insights and examples. The debt must be in registered form (i. shall determine the number and class of new partnership interests in the Partnership to be issued in respect of any such receipt and the terms and. A partner whose capital account is negative may still have a positive basis in his partnership interest because his share of partnership . Under this procedure, the partnership's books are closed on the exit date, and the tax items from the beginning of the tax year up to the exit date are totaled. Buy Download $347. It is a variation of the debt-equity ratio and gives the same indication as the debt-equity ratio. Sale of Equity Interest. Capital Accounts The Partnership shall establish and maintain a Capital Account for each Partner. negative ACB in partnership interests. might be negative. </p><p>This results in a negative. 1031 like-kind exchange; if the exchange is properly structured, some of the partners can trade their interests in the property distributed in Sec. A simple current rule of thumb is that tax equity accounts for 35% of the capital stack of a typical solar project, plus or minus 5%. The capital account is a record of each member's financial stake in the LLC, reflecting their capital contributions, additional contributions, and income or loss allocations. The "Adjusted Capital Account" of a Partner in respect of any Partnership Interest shall be the amount that such Adjusted Capital Account would be if such Partnership Interest were the only interest in the Partnership held by such Partner from and after the date on which such Partnership Interest was first issued. The following four accounting steps must be taken, in order, to dissolve a partnership: sell noncash assets; allocate any gain or loss on the sale based on the income-sharing ratio in the partnership agreement; pay off liabilities; distribute any remaining cash to partners based on their capital account balances. Assume that his tax basis capital account is negative $200,000 and his share of partnership liabilities is $300,000, and the. Partnership Tax Complications. The amount of the loss is the partner's basis in the property-generally his or her capital account balance increased by his or her share of partnership liabilities. A partner's gain from the sale of a partnership interest is generally eligible for taxation under the beneficial long-term capital gain tax rate. A partner whose capital account is negative may still have a positive basis if his share of partnership liabilities exceeds his negative capital account. A mortgage is a legal instrument of the common law which is used to create a security interest in real property held by a lender as a security for a debt, usually a mortgage loan. 755 allocation: (1) determine the FMVs of all partnership assets; (2) divide the assets into two classes consisting of capital gain property (which includes Sec. A partner's outside basis should never have a negative balance. The tax inquiry, however, is more involved, and the “retirement agreement” should seek to address as many tax issues as possible. capital accounts, with A's capital account reflecting A's $6 contribu-tion and B's capital account reflecting B's $4 contribution. The IRS’ interest in tracking these negative balances correlates to ensuring compliance with the requirements that (1) a partner must have sufficient basis in their partnership interest to utilize these losses on their personal returns and avoid capital gains on distributions, and (2) the partner generally must eventually recapture the. Differences in treatment of redemptions of partnership. here's a link to a worksheet you can use. It is likely that the partnership will have to provide a reconciliation between tax capital provided on Schedule K-1 and whatever accounting method is used (e. Interests in publicly traded partnerships (PTPs) can be a valuable part of an investor's portfolio, but because these investments are partnership interests, the tax reporting for them can be complex, and losses passed through by PTPs may be limited. 8 : Redemption and Repurchase of Units : 16 : 4. To the extent a partnership's business interest deduction is limited, the deferred business interest ("excess business interest expense") must be allocated to the partners, which reduces the partners' bases in their partnership interests. The partnership is terminated as of the sale. At the most elemental level, then, each owner’s. 3 percentage points improvement on the prior year, after absorbing net losses from Hurricane Ian ($40 million) and Ukraine ($34 million). However, a partner's capital account can be negative . In addition, many other LIHTC properties are having difficulties generating positive cash flow or significant tax benefits for their investors - either because of. 481(a) adjustment should be allocated among partners with varying interests during the four-year. The account earns $20 interest. TLM's capital account would be credited for $30,000 in this case. Targeted allocations involve a partnership's liquidating not in accordance with partner capital accounts but, instead, in accordance with a negotiated distribution waterfall. If a distribution of non‑cash property to a partner would cause a partner’s share of income and loss from assets that produce capital gain and loss to differ from the partner’s share of income and loss from hot assets, then Section 751 (b) of the Code applies. Complete Section J, indicating that at the end of the reporting period the partner's share of the profit, loss and capital accounts have all been reduced to zero. The underlying. If the contingent payment is less than the projected fixed amount, you have a negative. The tax treatment of redemptions of partnership interests is extremely complex and uncertain. The transferee partner gets an outside tax basis in the partnership equal to the purchase. (a) If at any time a Limited Partner or Assignee fails to furnish an Eligible Holder Certification or other information requested within th. For a fuller explanation of partnership journal entries, view our tutorials on partnership formation, partnership income distribution, and partnership liquidation. Generally, a partner does not recognize gain or loss upon contributions of property to a partnership in exchange for a partnership interest. The amount of the loss is the partner's basis in the property-generally his or her capital account balance increased by his or her share of partnership liabilities. Any negative adjustment made to the Carrying Value of an Adjusted Property as a result of either a BookDown Event or a Book- -Up Event shall first be deemed to offset or decrease that. 1 Appellants have not raised any arguments concerning the accuracy-related penalty for the 2011 tax year. Partnerships filing Form 1065 for tax year 2020 must calculate partner. ] 302(a) or [Sec. 2 million, +26% on a pro. The basis of the assets of a partnership or LLC may not reflect the basis of the interest in the hands of the partners(s). A partner’s tax basis capital account can be negative when its outside basis is zero or positive because outside basis is increased by the partner’s share of partnership liabilities under § 752 and the partner’s tax basis capital account is not. It contains well written, well thought and well explained computer science and programming articles, quizzes and practice/competitive programming/company interview Questions. It is important to note that the tax consequences of dissolving a partnership can be slightly different depending on how the assets of the partnership are distributed. 755-1(b)(5) 34. Earlier attempts left the market confused. Partnership Interest On Capital. William & Mary Law School Scholarship Repository | William & Mary Law. In a liquidation of the partnership, a partner that has agreed to a DRO must restore it (i. 15 oct. I'm assuming the reason for negative capital is that debt gave the partnership the ability to incur more in losses than was invested. His tax basis capital account is $(100,000), and his share of the partnership's liabilities is $150,000. The redemption rules generally allow the redeeming partner to recover full basis before recognizing any gain, unlike standard installment sale rules that require pro rata recognition. Shareholders' Equity = Equity Share Capital + Preference Share Capital + Reserves and Surplus (Excluding fictitious Assets) + Money received against share warrants. Dec 12, 2019 · A deficit restoration obligation, or “DRO,” is a promise by a partner to make a capital contribution to a partnership if the partner has a negative capital account when the partnership liquidates. In the case of sales of partnership interests, debt relief includes the decrease in the partner's share of partnership liabilities. Partnership Form Partner. 2 Rev. This means, generally, that tax consequences of transactions are taxed to the partners instead of at the entity level. To illustrate these concepts, suppose A is a member of partnership PRS in which the partners have equal interests in capital and profits. A must report gain or loss, if any, resulting from the sale of A's partnership interest in accordance with § 741. The partner can use the distributions received to repay the debt. Interest on Debentures; Redemption of Debentures; Redemption of Debentures: Meaning, Sources and Rules regarding Redemption;. . craigslist lexington north carolina, jordan lewis only fans, black pornsites, borntobefuck, tyga leaked, nike unisex hoops elite pro basketball backpack, videos of lap dancing, touch of luxure, mom sex videos, erotica smoking, ravin r29x problems, lightshot jumpscare link co8rr